Econometrics and Financial Data Modeling

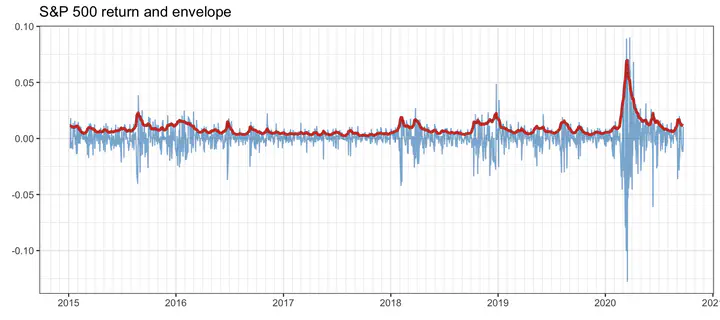

S&P 500 returns showing volatility clustering

S&P 500 returns showing volatility clustering

Financial time series — asset returns, volatility, intraday prices — exhibit rich temporal structure that the simple i.i.d. model fails to capture. Econometrics provides the statistical and mathematical framework for modeling returns conditioned on historical observations, with two central families of models: mean models (AR, ARMA, VAR, and state-space models via the Kalman filter) that describe the conditional expected return; and volatility models (GARCH and stochastic volatility) that capture time-varying conditional variance, including the well-documented phenomenon of volatility clustering.

A practical challenge is that financial data are heavy-tailed and often incomplete due to missing observations, illiquid assets, or asynchronous trading. Our research develops robust statistical estimation methods — for mean vectors, covariance and precision matrices, and model parameters — that remain reliable under Student-t and elliptical distributions with missing data, combining M-estimators, EM algorithms, and regularization for well-conditioned estimates in high-dimensional settings.

Software

Book

- Daniel P. Palomar, Portfolio Optimization: Theory and Application, Cambridge University Press, 2025.

Papers

-

Yifan Yu, Shengjie Xiu, and Daniel P. Palomar, “Robust Filtering and Learning in State-Space Models: Skewness and Heavy Tails Via Asymmetric Laplace Distribution,” accepted in IEEE Trans. on Signal Processing, 2026.

-

Chenyu Gao, Ziping Zhao, and Daniel P. Palomar, “Novel Penalty Methods for Maximum Likelihood Estimation of Gaussian and Student’s t GARCH,” accepted 2025, to appear in IEEE Trans. on Signal Processing, 2026.

-

Esa Ollila, Daniel P. Palomar, and Frédéric Pascal, “Affine equivariant Tyler’s M-estimator applied to tail parameter learning of elliptical distributions,” IEEE Signal Processing Letters, vol. 30, pp. 1017-1021, Aug. 2023.

-

Rui Zhou, Jiaxi Ying, and Daniel P. Palomar, “Covariance Matrix Estimation Under Low-Rank Factor Model with Nonnegative Correlations,” IEEE Trans. on Signal Processing, vol. 70, pp. 4020-4030, Aug. 2022.

-

Arnaud Breloy, Sandeep Kumar, Ying Sun, and Daniel P. Palomar, “Majorization-Minimization on the Stiefel Manifold with Application to Robust Sparse PCA,” IEEE Trans. on Signal Processing, vol. 69, pp. 1507-1520, Feb. 2021.

-

Esa Ollila, Daniel P. Palomar, and Frédéric Pascal, “Shrinking the Eigenvalues of M-estimators of Covariance Matrix,” IEEE Trans. on Signal Processing, vol. 69, pp. 256-269, Jan. 2021.

-

Rui Zhou, Junyan Liu, Sandeep Kumar, and Daniel P. Palomar, “Student’s t VAR Modeling with Missing Data via Stochastic EM and Gibbs Sampling,” IEEE Trans. on Signal Processing, vol. 68, pp. 6198-6211, Oct. 2020.

-

Junyan Liu and Daniel P. Palomar, “Regularized Robust Estimation of Mean and Covariance Matrix for Incomplete Data,” Signal Processing, vol. 165, pp. 278-291, July 2019.

-

Junyan Liu, Sandeep Kumar, and Daniel P. Palomar, “Parameter Estimation of Heavy-Tailed AR Model With Missing Data Via Stochastic EM,” IEEE Trans. Signal Processing, vol. 67, no. 8, pp. 2159-2172, April 2019. [R package imputeFin]

-

Ying Sun, Prabhu Babu, and Daniel P. Palomar, “Robust Estimation of Structured Covariance Matrix for Heavy-Tailed Elliptical Distributions,” IEEE Trans. on Signal Processing, vol. 64, no. 14, pp. 3576-3590, July 2016. [Matlab code]

-

Ying Sun, Prabhu Babu, and Daniel P. Palomar, “Regularized Robust Estimation of Mean and Covariance Matrix Under Heavy-Tailed Distributions,” IEEE Trans. on Signal Processing, vol. 63, no. 12, pp. 3096-3109, June 2015. [Matlab code] [R package fitHeavyTail]

-

Junxiao Song, Prabhu Babu, and Daniel P. Palomar, “Sparse Generalized Eigenvalue Problem via Smooth Optimization,” IEEE Trans. on Signal Processing, vol. 63, no. 7, pp. 1627-1642, April 2015. [Matlab code]

-

Yiyong Feng, Daniel P. Palomar, and Francisco Rubio, “Robust Optimization of Order Execution,” IEEE Trans. on Signal Processing, vol. 63, no. 4, pp. 907-920, Feb. 2015.

-

Mengyi Zhang, Francisco Rubio, Daniel P. Palomar, and Xavier Mestre, “Finite-Sample Linear Filter Optimization in Wireless Communications and Financial Systems,” IEEE Trans. on Signal Processing, vol. 61, no. 20, pp. 5014-5025, Oct. 2013.

-

Mengyi Zhang, Francisco Rubio, and Daniel P. Palomar, “Improved Calibration of High-Dimensional Precision Matrices,” IEEE Trans. on Signal Processing, vol. 61, no. 6, pp. 1509-1519, March 2013.

-

Francisco Rubio, Xavier Mestre, and Daniel P. Palomar, “Performance Analysis and Optimal Selection of Large Minimum-Variance Portfolios under Estimation Risk,” IEEE Journal on Selected Topics in Signal Processing: Special Issue on Signal Processing Methods in Finance and Electronic Trading, vol. 6, no. 4, pp. 337-350, Aug. 2012.